Knightian Uncertainty Dispatch — May 2026

Four new papers + two essentials on shifting forecast errors

Welcome to the sixth issue of the Knightian Uncertainty Dispatch — a monthly curated reading list for anyone thinking about macroeconomics, finance, and forecasting in a world where the future is not just risky, but sometimes genuinely unforeseeable because it may differ from the past.

Each month, I recommend four new papers + one “essential” that help grapple with structural change and uncertainty beyond probabilistic risk — and what those realities imply for economic modeling, forecasting, and policymaking.

The goal is to curate papers that:

Deepen our understanding of market outcomes and policy in a world with unforeseeable structural change and Knightian uncertainty.

Are useful for how we actually reason and forecast in unstable environments.

Connect to one another — so the pieces speak to each other rather than living in isolated silos.

This month’s theme is shifting forecast errors.

The April Dispatch and the posts behind it documented the institutional shift now underway in central-bank forecast communication: scenarios replacing fan charts, no designated central projection, robustness across scenarios written into the analytical framework of major central banks. That shift is a response to a problem that has been visible in the data for forty years and that the post-pandemic experience has made impossible to overlook. Forecasts produced by major institutions and market participants deviate from outcomes in systematic, regime-contingent ways. The deviations are not noise. They have structure. And the structure is not what the standard interpretations predict.

This issue is built around two institutional documents and two academic papers that, taken together, document the structure of the deviations clearly. The Sveriges Riksbank published its statutory Account of Monetary Policy 2025 on March 3. Two months earlier, Morten Ravn and Carolyn Wilkins delivered the fifth in a series of external evaluations of Swedish monetary policy that the Riksdag commissions roughly every five years, covering 2015–2024. Together, the two documents provide a public record of a major central bank’s forecast performance through the post-pandemic inflation surge and its aftermath. Stillwagon (2026) applies Bai-Perron structural break tests to the Coibion–Gorodnichenko forecast-error regression on US Survey of Professional Forecasters data; once breaks are allowed for, the constant-parameter regression’s conclusions reverse. Granziera, Jalasjoki, and Paloviita (2025) document the threshold-conditional form of the same finding for the ECB’s inflation forecasts — forecast bias is concentrated in regimes where inflation exceeds 1.8 percent and is invisible to averaged tests.

This issue includes two essentials: Zarnowitz (1984) and Lovell (1986) — the foundational empirical case, made when much of the profession doubted survey data could test the theory at all, that survey forecasts reject the rational expectations hypothesis and its prediction that forecast errors should be unpredictable. Both warned that structural change and Knightian uncertainty were the reason. Forty years on, we are still finding the same patterns, with sharper methods, at more institutions, and with new regimes to test them on. What has changed is what we can now say about the structure of the deviations.

The interpretive question the issue is built around is not whether forecasts deviate from outcomes in systematic ways. That has been settled empirically since Lovell and confirmed by a huge number of empirical studies. The question is what the systematic deviations mean.

The dominant accounts in the literature — information frictions (sticky information, noisy information, rational inattention) and behavioral biases (diagnostic expectations, extrapolation, overconfidence) — preserve the assumption that the data-generating process is stable and formalize the deviation from full-information REH with constant parameters (a loop I traced in detail in Fixed Models in a Changing World). That implies that the systematic components in forecast errors should be the same over time.

The Riksbank record, the Stillwagon evidence, and the Granziera state-dependence finding together suggest a different reading. The systematic components in forecast errors are themselves regime-shifting, in a way that no constant friction and no constant bias can account for. They are what one would expect if the underlying process undergoes unforeseeable change — and if rational expectations have to be reformulated to accommodate such change rather than abstracting from it.

Paper #1: The Riksbank’s Account of Monetary Policy 2025

Document: Account of Monetary Policy 2025, Sveriges Riksbank, published March 3, 2026. The Riksbank’s annual statutory ex-post accountability report to the Riksdag Committee on Finance. Link.

The Account is the Riksbank’s annual public reckoning with its own monetary policy — a statutory ex-post evaluation tied to a parliamentary hearing and complemented by an every-five-years external evaluation (the Ravn–Wilkins report below is the latest). Few central banks evaluate their own forecasting record this systematically: the ECB does so in occasional Economic Bulletin boxes rather than a dedicated report, and the Bank of England began a comparable standalone Forecast Evaluation Report only in January 2026, following the Bernanke review. The 2025 Account covers a year that took the policy rate from 2.50 to 1.75 percent across three cuts.

The first sections of the Account are largely a record of what the Bank has done over the year. The document opens for the first time with a freestanding Executive Board commentary that reaches for Knightian uncertainty language: tariffs “on a scale not seen since the mid-1930s,” “worrying cracks in the rule-based world order that had prevailed since the end of the Second World War,” “longer-term effects ... remain unclear.” The analytical core of the document, for the Dispatch’s purposes, is Section 3.

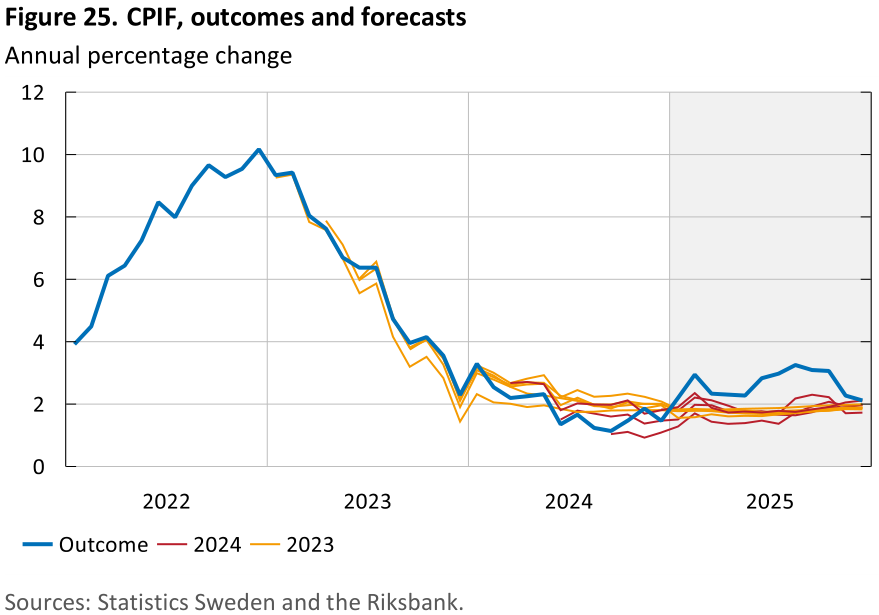

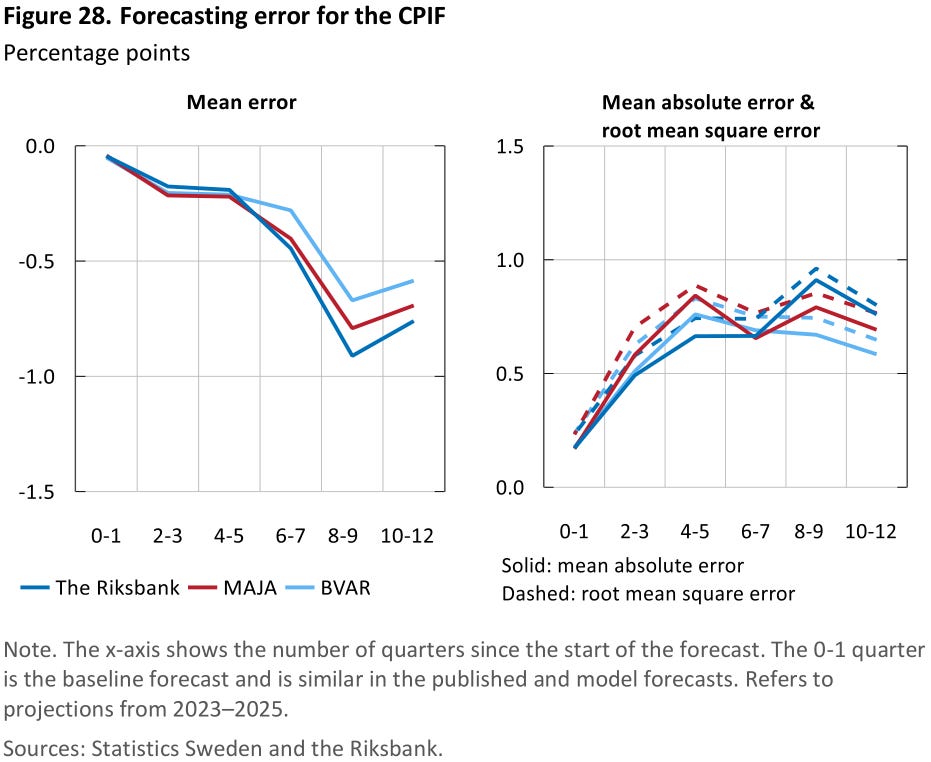

What the Account shows. The CPIF inflation forecasts the Riksbank produced in 2023 and 2024 sit systematically below the inflation that actually materialized in 2025 (see Figure 25 below). The under-prediction is modest in absolute terms — Swedish inflation in 2025 was within striking distance of the target — but it is one-directional and persists across vintages and across the year. Figure 28 adds a second feature: decomposed by horizon, the errors are signed in the under-prediction direction at every horizon and grow as the horizon lengthens. The Account treats the horizon growth as the salient finding, noting that the judgment-augmented Riksbank forecast carries more long-horizon bias than the underlying MAJA (the Bank’s flagship DSGE) and BVAR model forecasts, and recommends placing greater weight on the model forecasts at long horizons.

A structural-change reading. The observation that matters most is not the horizon growth the Account emphasizes but the persistence it passes over. Under the standard theoretical assumption that the economy’s structure is fixed — the assumption on which MAJA and the BVAR both rest — forecast errors should be unpredictable: mean-zero, with no systematic sign. A run of one-directional errors that persists across an entire episode is precisely the pattern that assumption rules out. It is, however, exactly what one expects when a model estimated with constant parameters is used in an economy whose parameters have shifted: the constant estimates are, in effect, an average over the distinct regimes in the sample, so in any regime that sits away from that average the model is biased in one direction and stays biased for as long as the regime lasts. The horizon growth then follows as a symptom of the same cause rather than an independent fact. A constant-parameter model mean-reverts to its estimated steady state at its estimated speed — here, toward the 2 percent target. The current regime may differ on either margin: a different anchor, or a slower convergence to it. Since the anchor is ultimately the fixed target, the live margin is the convergence rate — so the forecast is pulled back to target faster than the regime warrants, and the bias grows with the horizon.

The judgment-helps-on-average finding. Section 3.2 concludes that, across all forecasted variables for the studied period, “judgement has, on average, contributed to more accurate forecasts” (page 47) — though not for inflation, where judgment adds to the long-horizon bias rather than reducing it (Figure 28). It is the rare case in which an institution publicly weighs its own judgment against its model, and the result is telling. Judgment is where the forecasters’ reading of the current regime enters: how the situation differs from the past, what has changed recently, where the conjuncture seems to be heading. The models, by the fixed-structure assumption, cannot represent any of this — they carry forward the average parameters of the estimation sample. So the fact that adding judgment improves the forecasts on average is itself a symptom that the models are missing the regime change.

The forecast errors in two figures

Figure 25 records the systematic component over the year; Figure 28 decomposes the errors by horizon and compares the judgment-augmented Riksbank forecast against the underlying model forecasts.

Figure 25: CPIF forecasts produced in 2023 and 2024 against the inflation that materialized in 2025. The forecasts sit systematically below the realized path throughout the year.

Figure 28: CPIF forecast errors by horizon. The errors are signed in the under-prediction direction across all horizons and grow with the horizon. The judgment-augmented Riksbank forecast carries more long-horizon bias than the underlying MAJA (DSGE) and BVAR model forecasts.

Reprinted from Sveriges Riksbank, Account of Monetary Policy 2025.

Why I’m recommending it

The Account is a detailed public record of a major central bank’s recent forecast performance, with judgment-augmented forecasts compared against MAJA and BVAR forecasts at horizons of 0 to 12 quarters.

Figures 25, 26, and 28 document systematic, persistent under-prediction of 2025 inflation that the Account narrates as a horizon issue but that I read as a symptom of models that do not account for unforeseeable change.

The page-47 finding that judgment helps on average is the clearest public statement from inside an institution that the judgment can improve model forecasts.

The takeaway

The 2025 record shows that the same constant-parameter model and the same judgment apparatus that the Riksbank was using before the post-pandemic period continue to produce systematic forecast errors, smaller in magnitude than in 2021–22 but still patterned. The recommendation to weight the model more heavily at long horizons accepts the constant-parameter model as a suitable theoretical framework. The deeper question — whether constant-parameter models are appropriate for forecasting and policy analysis in a changing world — is not asked.

If you only read a few pages

Read Section 3 in full. Figures 25 and 26 are the systematic-component record. Figure 28 is the horizon decomposition. Page 47 carries the “judgment helps on average” finding. The Executive Board commentary in Section 1 is worth a quick read for the Knightian-flavored passages.

Paper #2: Ravn and Wilkins on the Riksbank’s Forecast Performance

Document: Riksbank Evaluation, 2015–2024 by Morten Ravn (University College London) and Carolyn Wilkins (Princeton; former Bank of Canada Senior Deputy Governor; current Bank of England Financial Policy Committee external member). Commissioned by the Finance Committee of the Sveriges Riksdag, delivered January 12, 2026. Link.

The Ravn–Wilkins report is the fifth in the series of independent external evaluations of Swedish monetary policy in a longer-term perspective that the Riksdag Committee on Finance has commissioned since the mid-2000s. At 146 pages, ten chapters, and seventeen recommendations, it is the most comprehensive external evaluation of any major central bank’s monetary policy in 2026. The headline assessment is that the Riksbank acted with determination in difficult circumstances and that targeted reforms are warranted rather than a wholesale redesign of the framework.

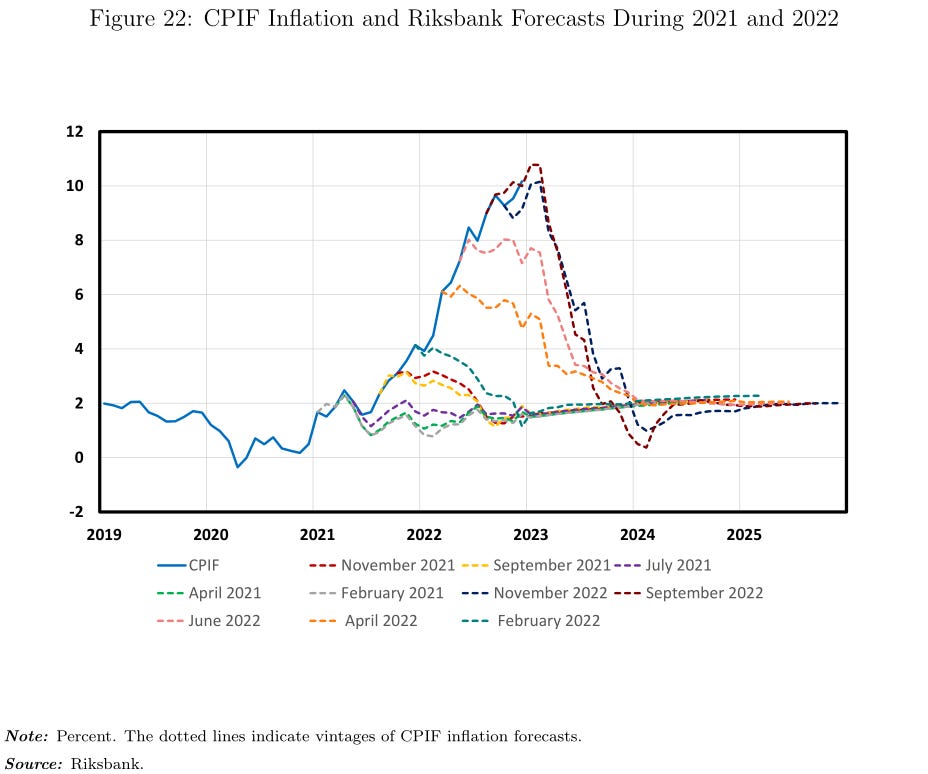

Chapter 6, on forecast performance, is the most relevant part for this Dispatch. Figure 22 shows the Riksbank’s CPIF inflation forecasts made through 2021 and 2022 against the realized path: the forecasts sit far below realized inflation throughout the surge, predicting a steady return to the 2 percent target while inflation kept climbing, with under-predictions that were large and sustained over many quarters. And the Riksbank was not alone. The 2021–22 inflation surge was a global phenomenon, and the report’s cross-country comparison shows that forecast errors of this kind — large, one-directional, and persistent — hit virtually every major central bank. This was a period of major structural change, in supply chains, energy and labor markets, and the pricing behavior of firms; it is the most important recent example of a forecast breakdown caused by unforeseeable structural change.

What the evaluation says went wrong. Chapter 6.3.2 is direct about why MAJA — the Riksbank’s flagship DSGE model — broke down. Because MAJA is fitted to historical data, the report notes, “it is aimed at accounting for economic circumstances that have been observed in the past,” and so “is unlikely to properly account for unusual circumstances that have rarely been observed in the data.” The chapter then itemizes the assumptions that failed: linear exchange-rate pass-through, against documented threefold asymmetry across inflation regimes (Linderoth and Meuller 2024 find 17.4 percent pass-through in high-inflation regimes versus 6.9 percent in low-inflation regimes; MAJA is linear); a fixed Calvo price-setting frequency, against the faster pass-through documented for 2021–22 (Klein, Strömberg, and Tysklind 2024); mean-reverting inflation forecasts; and symmetric, linear shock responses around a steady state. The report cites Leeper (2003) on DSGE models missing “structural uncertainty,” and Iversen, Laséen, Lundvall, and Söderström (2016) on Riksbank DSGE underperformance during structural breaks, when judgmental overlays come to dominate the model’s own output.

A comment. The evaluation sees the problem clearly. It does not treat 2021–22 as bad luck — it even diagnoses the policy conduct of those years as “fighting the last war” — and it states plainly that “the priority now is to adapt [the Riksbank’s] tools to an environment in which large shocks and structural breaks may be more common” (page 9). Where I would push further is on what adapting the tools requires. The fixes the report recommends — make pass-through nonlinear, recalibrate Calvo, allow some asymmetry, lean more on scenarios — each relax one assumption at a time, but all of them keep the model’s parameters constant; they make a fixed structure a little richer rather than letting the structure change. That is the same constant-parameter assumption behind the Account’s persistent 2025 misses in Paper #1. Taking unforeseeable change seriously means building it into the formulation of the model itself, and estimating its parameters while continuously testing for structural change rather than assuming them to have been constant without testing this crucial assumption. I set out the policy side of this in the April Dispatch and the forecasting side in Five Principles for Forecasting in a Changing Economy.

There is a further reason to take that deeper move seriously. The report reads 2021–22 as an extraordinary episode. Indeed it was. But “extraordinary” implies a normal to return to, and events since publication cut against that reading. The Iran war and the surging energy prices that followed it arrived only weeks after the evaluation appeared. The world has not settled back into the pre-2021 regime, it has moved into another one. If structural breaks are a recurring feature of the environment rather than rare departures from a stable structure, then opening models and forecasting practice to unforeseeable change is not a contingency plan for the next crisis. It is the normal case.

The forecasts vs. realized inflation in one figure

Figure 22, from Chapter 6, is the 2021–22 counterpart to the Account’s 2025 record.

Figure 22: Riksbank CPIF inflation forecasts made in 2021 and 2022 against the realized path. The forecasts sit far below realized inflation throughout the surge — the models predicted a return to the 2 percent target while inflation kept rising.

Reprinted from Ravn and Wilkins (2026), Riksbank Evaluation 2015–2024.

Why I’m recommending it

Chapter 6.3.2 is the most detailed external evaluation of a major central bank’s monetary policy in 2026, and it names the specific structural-stability failure mode of its flagship DSGE model: linear pass-through, fixed Calvo, mean-reverting forecasts, symmetric responses.

The 2021–22 surge is the most important recent example of a forecast breakdown caused by unforeseeable structural change, and the report shows it was no Swedish idiosyncrasy: errors of the same kind — large, one-directional, persistent — hit virtually every major central bank. It is the cleanest available case of constant-parameter forecasting failing systematically when the structure shifts.

Reading the report alongside the Account gives the closest thing available to a controlled comparison: same model, same institution, same forecasting apparatus, two episodes of systematic under-prediction with very different magnitudes. The pattern is the empirical signature the literature has been chasing for forty years.

The takeaway

Ravn and Wilkins diagnose the forecast breakdown clearly and with independent scholarly authority: they grant that MAJA works in normal times but not in unusual ones, and they call for adapting the Riksbank’s tools to a world of more frequent structural breaks. The fixes they propose stay within the constant-parameter framework — which is why the evidence the report collects supports a deeper reading than the evaluation itself reaches for.

If you only read a few pages

Read Chapter 6 in full. Section 6.2 with Figure 22 carries the 2021–22 forecast record, and the report’s international comparison shows the same breakdown across central banks. Section 6.3.2 explains why MAJA broke down. Section 6.3.3 is the scenarios discussion. Recommendation 3.3 — institutionalize scenarios as a decision device — is in Chapter 10.

Paper #3: Stillwagon on Structural Breaks in Forecast-Error Regressions

Paper: “Professional forecasters do not commit timeless errors: Evidence from structural breaks in tests of over-reaction” by Joshua R. Stillwagon. Economics Letters, vol. 263, article 112939, 2026. Link.

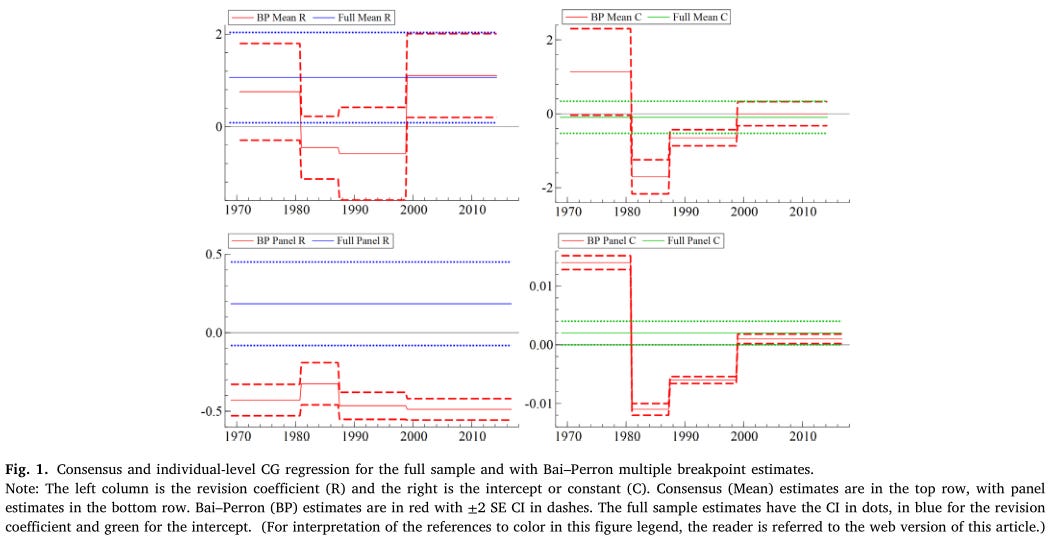

Stillwagon applies Bai-Perron structural break tests to the Coibion–Gorodnichenko (2015; CG) forecast-error regression using the longest-running Survey of Professional Forecasters inflation series — the GDP deflator — over 1969–2016, ending in 2016 to match the sample of Bordalo, Gennaioli, Ma, and Shleifer (2020; BGMS). The CG regression is the workhorse of the modern forecast-error literature. It regresses the consensus or individual forecast error on the prior forecast revision. The rational expectations hypothesis predicts that the coefficient on the revision should be zero when implemented in a constant-parameter model with full information. CG’s full-sample finding is a significantly positive coefficient at the consensus level — interpreted as the canonical evidence for information rigidity. BGMS, at the individual level, find a negative coefficient — interpreted as the canonical evidence for diagnostic-expectations over-reaction. The literature treats both as stable structural features of expectation formation.

The result of allowing for structural breaks reverses both conclusions (Figure 1). At the consensus level, the full-sample finding of under-reaction holds only post-1999. Earlier subsamples show insignificant revision coefficients but significant, time-varying intercepts. At the individual forecaster level, break-adjusted regressions reveal consistently negative revision coefficients across all regimes at the 1 percent significance level — completely reversing the full-sample conclusion that masked over-reaction by averaging across regimes. The estimated breaks align with Federal Reserve leadership changes, suggesting that genuine uncertainty about novel policy regimes drives forecast errors.

The title says exactly what matters: forecast errors are not timeless. The systematic component shifts at regime boundaries. The paper is an academic complement to the Riksbank record. Where the Account and external evaluation document two episodes of under-prediction with very different magnitudes in the same institution’s inflation forecasts, Stillwagon documents the same kind of regime-contingent structure formally across half a century of US survey data.

A comment. The standard readings of these regressions — information rigidity (CG 2015) and diagnostic over-reaction (BGMS 2020) — share a hidden premise: that the data-generating process is constant and the deviation from FIRE can itself be represented with a constant parameter. Stillwagon’s empirical findings refute that premise: the parameters of the forecast-error regressions are not constant. But the deeper point is the one Roman Frydman and I make in our working paper and in the revision we are completing: FIRE implemented in a constant-parameter model cannot represent the expectations of rational market participants, because it abstracts from the unforeseeable change those participants actually face. Once the economy can move to a regime that has not yet been observed, model-consistent expectations no longer imply unpredictable forecast errors. Instead, they imply the systematic, regime-shifting components we and Stillwagon document.

Full-sample vs. break-adjusted estimates in one figure

Figure 1 is the argument in one picture: the single full-sample estimate set against the regime-specific estimates the breaks reveal.

Figure 1: The Coibion–Gorodnichenko revision coefficient, estimated over the full sample versus over the break-adjusted subsamples. The single full-sample number masks regime-specific estimates that differ across periods — the constant coefficient is an average over distinct regimes.

Reprinted from Stillwagon (2026).

Why I’m recommending it

The paper is a current academic complement to the Riksbank record. Same kind of finding — regime-contingency in the systematic component of forecast errors — produced with a different econometric method, on a different sample, over a much longer horizon.

The empirical results is a direct empirical refutation of the methodological premise behind both the CG (2015) information-rigidity interpretation and the BGMS (2020) diagnostic-expectations interpretation.

The empirical results suggest that accounting for survey-based expectations requires acknowledging the importance of unforeseeable structural change.

The takeaway

Forecast errors are not timeless. The systematic component shifts over time. Accounting for survey-based forecast errors requires acknowledging unforeseeable structural change.

If you only read a few pages

Read Section 3 for the consensus-level results and Section 4 for the individual-level results. Figure 1 shows the full-sample versus break-adjusted estimates side by side.

Paper #4: Granziera, Jalasjoki, and Paloviita on State-Dependent ECB Forecast Bias

Paper: “The Bias of the ECB Inflation Projections: A State-Dependent Analysis” by Eleonora Granziera (Norges Bank), Pirkka Jalasjoki (Bank of Finland), and Maritta Paloviita (Bank of Finland). Journal of Forecasting, vol. 44, no. 3, pp. 922–940, 2025. Link.

Granziera, Jalasjoki, and Paloviita test for state-dependent bias in ECB inflation projections using the Odendahl–Rossi–Sekhposyan (2023) threshold regression approach. Linear, full-sample tests find ECB forecasts unbiased on average. The state-dependent tests reveal systematic under-prediction when observed inflation exceeds an estimated threshold of 1.8 percent — close to the ECB’s de facto target — with bias peaking at intermediate horizons (one to four quarters ahead) and ranging from 0.10 to 0.37 percentage points. The bias cannot be explained by errors in conditioning assumptions for interest rates, exchange rates, or oil prices.

The 2021–22 surge is excluded — and the result survives. The baseline analysis deliberately strips the largest forecast errors out of the sample as outliers: the vintages of the Great Financial Crisis, the COVID shock, and the 2021–22 surge are all dropped (see Table A1). The state-dependent under-prediction is therefore not an artifact of the extreme episode — it is identified off ordinary above-target quarters, because the estimated 1.8 percent threshold is low enough that most non-crisis periods sit above it. As the authors put it, the bias “is the result of systematic underprediction by the ECB even at times when inflation does not substantially overshoot the target” (p. 923), and it holds even when the entire post-2019 sample is removed.

This is the piece that completes the picture in this issue. Ravn and Wilkins document the Riksbank under-predicting through the 2021–22 surge; the Account finds the same under-prediction in the much milder 2025 episode; Stillwagon finds the systematic component of US professional forecasters’ errors shifting across half a century; and Granziera, Jalasjoki, and Paloviita find it at the ECB with the surge taken out altogether — in the ordinary above-target quarters that came before and around it. These systematic forecast errors are not a one-off event. They appear across central banks and professional forecasters, and they shift over time — which is what a regime-shifting process produces, and what a fixed bias or a one-off shock does not.

In one quote

The ECB systematically underpredicts inflation when inflation is high, which results in projections converging to target too quickly.

Granziera, Jalasjoki, and Paloviita (2025), p. 937.

Why I’m recommending it

The paper documents the threshold-conditional form of the finding that the Riksbank record and Stillwagon establish from different angles. Three independent econometric approaches, two central banks and professional forecasters, one phenomenon.

The paper documents a systematic bias in the ECB forecasts that occurred not only during the 2021-22 inflation surge, and which is invisible in the linear and constant form that averages across the entire sample.

The Odendahl–Rossi–Sekhposyan threshold regression is one of the central tools the modern forecast-evaluation literature is now using to detect regime-contingent bias that averaged tests miss.

The takeaway

ECB projection bias is not constant. It is concentrated in periods where inflation exceeds 1.8 percent.

If you only read a few pages

Read Section 3 for the threshold regression results and Table 1 for the contrast between linear and state-dependent bias estimates. Figure 1 shows the inflation states and projection distributions. Figure 2 (the bias curve as a function of the inflation state) is the cleanest single visualization of the state-dependent bias. Section 5.2 shows that standard models exhibit the opposite-sign bias.

The Essentials: Zarnowitz (1984) and Lovell (1986) on Testing Expectations with Survey Data

Papers: “Business Cycle Analysis and Expectational Survey Data” by Victor Zarnowitz. NBER Working Paper No. 1378, June 1984. Link. And “Tests of the Rational Expectations Hypothesis” by Michael C. Lovell. American Economic Review, vol. 76, no. 1, pp. 110–124, March 1986. Link.

Forty years ago, testing the rational expectations hypothesis against survey data was a contested move. The objection was methodological: expectations are not observed, so — in Edward Prescott’s words, quoted by Lovell — “surveys cannot be used to test the rational expectations hypothesis.” Zarnowitz and Lovell rejected that view and built the case that survey forecasts are exactly the right instrument for testing theoretical representations of expectations. Lovell held that direct testing of the hypothesis is “an appropriate and worthwhile activity”; Zarnowitz, that “it is not good ‘positive economics’ to dismiss [the survey evidence] on the ground that only theories, not their assumptions, can be tested.” The two papers are complementary in coverage — Zarnowitz examines professional forecasters (the Livingston and ASA-NBER surveys), Lovell the anticipations of firms and households (sales, inventories, prices, wages) alongside government forecasts — so that together they survey the whole field. The skepticism they argued against is long gone: a vast modern literature now does exactly what they advocated (see Coibion, Gorodnichenko, and Kamdar 2018 for a review).

Both papers show how regressions of actuals and survey forecasts can be used to test different theoretical representations of expectations as specific restrictions on the parameters. They were not the first to evaluate expectation representations this way: the framework descends from Mincer and Zarnowitz (1969). What followed was an enormous literature that extended these regressions in every direction and proposed new representations of expectations — sticky information, noisy information, diagnostic expectations — to account for what the tests kept finding.

What the tests kept finding is that the (full-information) rational expectation hypothesis’ prediction of unpredictable forecast errors is rejected by the data, most decisively for inflation. Using the ASA-NBER survey, Zarnowitz finds that roughly 70 percent of individual inflation forecasts fail the unbiasedness test and two-thirds fail the test for serially uncorrelated errors, against about 20 percent for real output. His verdict: “the great majority of inflation predictions since the late 1960s fail the rationality tests and show a strong underestimation bias,” for experts and agents alike. Lovell, reviewing the firm and household evidence, reaches the same conclusion (quoted below). Decades of work since have confirmed it — and yet a great deal of macroeconomic theory still rests on the hypothesis these papers showed the data reject.

Most striking, reading the two papers now, is the explanation they offered and that the literature then forgot. Both located the problem in structural change and genuine uncertainty. Zarnowitz is explicit: the rational expectations hypothesis presumes a stationary environment that agents have had time to learn, so that “unlike in Knight, 1921, or Keynes, 1936, there is no uncertainty here as to what the applicable objective probability disturbances are.” In a world of structural change, he argued, “uncertainty in the sense of Knight and Keynes is prevalent,” and the right notion of rationality is the effective use of “the limited available knowledge and information” in the face of an inherently uncertain future. Lovell, more cautiously, noted that departures from rationality “may be a transient phenomenon arising because economic actors are learning to adapt to a shift in regimes.” The literature that followed kept the rejection but set the diagnosis aside — formalizing the deviation from rationality with fixed parameter inside a stable model, rather than as the rational response to a changing one.

In two quotes

“the weight of empirical evidence is sufficiently strong to compel us to suspend belief in the hypothesis of rational expectations” — Lovell (1986)

“In a nonstationary world with structural changes and a mixture of random and autocorrelated disturbances, uncertainty in the sense of Knight and Keynes is prevalent.” — Zarnowitz (1984)

Why these are the essentials

They are the foundational empirical case that survey forecasts can and should be used to test theories of expectations — made when much of the profession doubted it could be done at all. The entire modern forecast-error regression literature, including the four new papers in this issue, descends from the argument these two papers won.

They reached, with the tools of the 1980s, the conclusion that the (full-information) rational expectations hypothesis is rejected by survey forecasts, most decisively for inflation — a finding confirmed by four decades of work since.

They named the reason — structural change and Knightian uncertainty — and proposed that rationality be understood as the effective use of limited knowledge under genuine uncertainty. That diagnosis was largely forgotten. Recovering it is what this issue is about.

The takeaway

Zarnowitz and Lovell established forty years ago that survey forecasts reject the full-information rational expectations hypothesis, and warned that structural change and Knightian uncertainty were the reason. The literature kept the rejection and forgot the warning, formalizing the deviation with a constant parameter inside a stable model. The four new papers suggest that the deviation is not constant.

If you only read a few pages

In Zarnowitz, read Section 2 (the critique of rational expectations) and Section 5 (the concluding observations), with Table 2 for the rejection rates. In Lovell, read Sections I–II for the framework and the evidence, and Section IV — “Should the Facts Be Allowed to Spoil a Good Story?” — for the assessment.

Closing Remarks

That’s it for the May issue of the Knightian Uncertainty Dispatch.

We have known for forty years that survey forecasts reject the full-information rational expectations hypothesis. Zarnowitz and Lovell established it in the mid-1980s — and both warned that the reason lay in structural change and uncertainty of the kind Knight and Keynes described.

The literature kept the rejection and set the warning aside. It explained the deviations from rationality by adding frictions — sticky information (Mankiw and Reis 2002), noisy information and rational inattention (Sims 2003; Woodford 2003), the forecast-error-regression revival (Coibion and Gorodnichenko 2015) — or behavioral biases — diagnostic expectations (Bordalo, Gennaioli, and Shleifer 2018) and extrapolation. Each of these deviations from REH’s perfect-foresight benchmark under full information is formalized with constant parameters in models that maintain the assumption that the economy’s structure is fixed. The future is assumed to be a probabilistic replica of the past. Frictions or behavioral biases lead to exactly the same systematic components in forecast errors over time.

The four papers in this issue are the evidence that the systematic components in forecast errors are not constant. The Riksbank’s own forecasts under-predict inflation by a margin that shifts with the regime; Stillwagon shows the Coibion–Gorodnichenko coefficient breaks at regime boundaries; Granziera, Jalasjoki, and Paloviita show the ECB’s bias is concentrated in regimes far from target and invisible to averaged tests. The systematic component of forecast errors is itself regime-shifting — which is exactly what a constant friction or a constant bias cannot represent.

Roman Frydman and I read this differently. The empirical evidence from forecast-error regressions does not reject the presumption that market participants are rational. It rejects the assumption that the economy’s structure is fixed — the assumption that the future is merely a probabilistic replica of the past — that REH rests upon. In other words, full-information REH is not an adequate theoretical representation of rational market participants’ expectations, because it abstracts from the unforeseeable change that they actually face.

Once we acknowledge that the economy can shift to a new regime that has not yet been observed, rational participants — using all the information available to them — will still produce forecasts that deviate from outcomes in systematic, regime-shifting ways. The shifting systematic component is not a failure of rationality or a defect of information processing; it is the unavoidable consequence of unforeseeable change. That is the answer to the question this issue opened with — what the systematic deviations mean — and it points to a constructive task: take unforeseeable change seriously by building it into our theoretical models and into how we forecast.

Building unforeseeable change into a model and representing expectations as consistent with such change alters the notion of rational expectations itself. They shift over time, in anticipation of and in response to unforeseeable change in the economy; they deviate from outcomes even when participants have full information; they differ across participants even when those participants share the same information; and they are shaped in part by psychological factors. My Substack series Rational Expectations Under Knightian Uncertainty develops this — how opening a model to unforeseeable change reshapes model-consistent expectations and, with them, what rational expectations are.

Roman Frydman and I presented the framework in two working paper in 2025. The first, Rational Expectations of Inflation Undergoing Unforeseeable Change, shows how to open economic models to unforeseeable change and represent participants expectations as consistent with such change. The second, Unforeseeable Change in Rational Participants’ Inflation Expectations, applied it empirically to forecast-error regressions. We are currently finalizing a substantially revised version of the latter. It uses two complementary break-detection methods — Bai-Perron and indicator saturation with Autometrics — to identify the nonrepetitive parameter shifts in U.S. Survey of Professional Forecasters forecast errors that constant-parameter REH and Markov-switching FIRE both rule out. The patterns this Dispatch documents — at the Riksbank, in the academic literature, and at the ECB — are exactly what that framework predicts.

If you have suggestions for papers I should cover in future issues — especially work that connects structural change, Knightian uncertainty, and real-world forecasting and policymaking — please send them my way.

And if you found this Dispatch useful and want the next issue in your inbox, consider subscribing. It helps the Dispatch reach the people who are interested in developing economic theory, policy analysis, and practical forecasting tools for a changing world characterized by Knightian uncertainty.